Retirement is not one date on a calendar. It is a long story made of smaller chapters, first job, first savings goal, family moments, career turns, health shifts, and the quiet math of time passing. If you treat those chapters as milestones you can plan for, you stop guessing and start steering. The best part is that you do not need perfect knowledge. You need a steady way to measure progress, and a habit of revisiting your timeline.

Key takeawayRetirement planning works best when it follows real life milestones. Map your timeline by age, career stage, and responsibilities. Set one money target, one time target, and one health target per season of life. Use time tools to make the plan feel real: a birthday countdown for motivation, alarms for habits, a timer for focus, a stopwatch for workouts, and a time calculator for long range date math. Review quarterly, adjust calmly, and keep moving. |

Mini quiz to match your milestone style

|

Answer eight questions, then get a short profile plus a suggested next step. This quiz runs in the page and keeps your answers on your device. |

What retirement really means in a timeline

Most people picture retirement as a finish line. That picture can cause two problems. One, it makes retirement feel far away. Two, it makes planning feel like a huge task that belongs to future you. A better picture is a timeline with checkpoints. Each checkpoint has a money task, a life task, and a time task. The money task builds your safety. The life task reflects what matters to you. The time task turns a vague goal into something you can measure.

Time.you is made for measuring time with clarity. It gives accurate time across time zones, down to the second, based on atomic clock synchronized time. That matters more than it seems. When you plan long range milestones, you need dates you can trust. When you build habits, you need consistent reminders. When you coordinate with family across cities, you need time zone confidence. All of that supports calmer retirement planning.

A simple milestone map that works for real people

Think of your life in seasons, not in perfect decades. Seasons change when responsibilities change. Education ends, work begins. Rent becomes a mortgage. You take care of children, parents, or both. Health needs evolve. Your plan should shift with the season.

| Season | Money focus | Time focus | Life focus |

|---|---|---|---|

| Starting out | Build emergency savings and reduce expensive debt | Set routines and track habit streaks | Learn skills, choose values, build support |

| Growth years | Raise savings rate and begin long term investing | Plan yearly reviews and weekly check ins | Career direction, relationships, housing choices |

| Responsibility peak | Protect with insurance and focus on retirement contributions | Manage calendars, deadlines, and family logistics | Caregiving, education costs, work stability |

| Pre retirement | Clarify retirement date, stress test budget, reduce risk | Count down to retirement date and key decisions | Health plan, purpose plan, housing plan |

| Retirement living | Spend with intention and protect against surprises | Use routines to keep mind and body active | Community, meaning, flexibility, joy |

This table is not a rule. It is a prompt. You can be in more than one season at the same time. You can also move between seasons more than once. The key is to match your actions to your actual life, not to a generic age.

Retirement milestones that show up before you expect them

Many retirement decisions arrive quietly. A friend talks about investing and you feel behind. A job offer asks you to move. A family member needs help. A health issue changes priorities. A market drop shakes your confidence. A timeline helps you respond without panic.

| Milestone moment | What it changes | One helpful action |

|---|---|---|

| First steady income | Choices become habits fast | Automate saving on payday |

| First big debt | Cash flow gets tight | Pick a payoff method and track dates |

| First dependent | Risk and responsibility rise | Review insurance and emergency fund target |

| Career plateau | Income growth may slow | Plan skill upgrades with a schedule |

| Caregiving begins | Time becomes scarce | Plan weekly blocks for admin and rest |

| Pre retirement window | Decisions have bigger impact | Set a review cadence and reduce surprises |

Start with a retirement date, then work backward

Picking a date can feel scary. It also makes planning easier. A date turns retirement into a project you can manage. If you cannot choose a single date, pick a range, then test it. A simple way to test is to write down what must be true by that time. That list becomes your milestones.

Working backward means you decide what needs to happen in the last five years, then the five years before that, then the next year. This approach keeps you from focusing only on distant goals. It also highlights bottlenecks early, like high fixed costs or lack of an emergency buffer.

For clean date math, the time calculator helps you add and subtract time spans without mental friction. You can map a target retirement month, then count back for decisions like downsizing, paying off a loan, or shifting to a lower stress role.

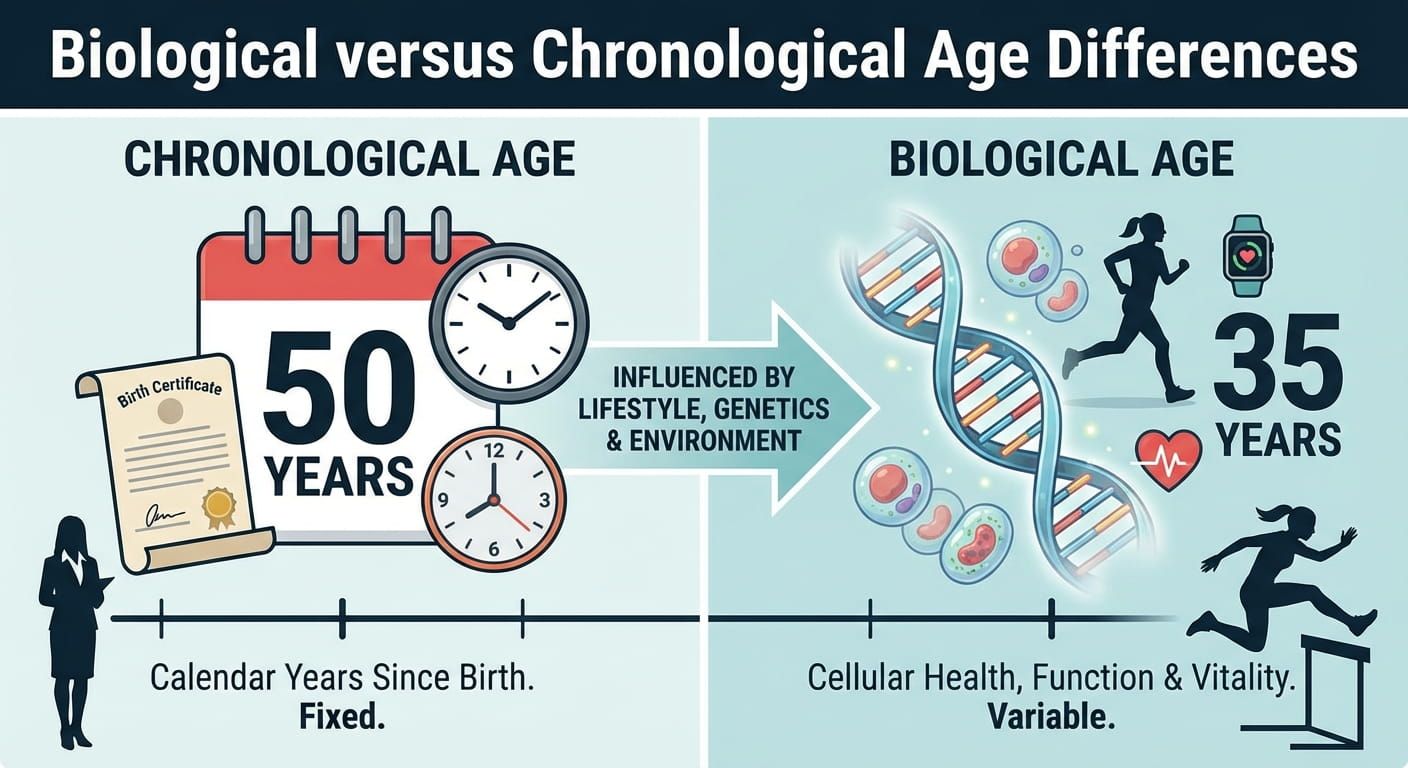

How to measure your age in ways that matter

Chronological age is your time since birth. It matters for official rules and typical milestones. Biological age is a different idea. It points at how your body is doing relative to your calendar age. For retirement, both matter. Chronological age can drive eligibility, while biological age shapes what kind of retirement you can enjoy.

If you want a deeper read on how those concepts differ and why people react strongly to each, biological vs chronological age is worth your time. It can help you plan health habits with the same seriousness as money habits, since both are part of the retirement picture.

At a practical level, get your current age accurate, then track meaningful points. You can use age to confirm your exact age based on your birth date and today’s date, then build a milestone plan from there.

Life milestones that shape your retirement plan

Retirement planning is personal. The numbers are important, but your milestones give the numbers meaning. Here are the milestones that tend to reshape the plan, even for people who do not think about retirement much yet.

- Leaving school and earning your first income. This is where habits start. Automatic saving is your friend.

- Moving out and paying full living costs. Rent, food, transport, and bills teach your true cost of life.

- Committing to a partner or shared household. Shared goals need shared timelines, even if money stays separate.

- Buying a home or signing a long lease. This often locks in fixed costs, which affects how early you can retire.

- Having children or taking on caregiving. Time and money pressure often peak here, so the plan must stay realistic.

- Hitting a career pivot point. Promotions, layoffs, industry shifts, and burnout change the future curve.

- Health changes. Your energy, mobility, and stress tolerance can shift, so timelines need revisiting.

- Approaching official retirement thresholds. Rules, benefits, and work choices start to matter more.

Even if you are young, these milestones arrive faster than expected. That is why a timeline, updated often, beats a perfect plan that you never revisit.

Using time tools to make long range goals feel real

Goals feel unreal when they live only in your head. Time tools turn them into visible, repeatable actions. That is why a time site can be part of retirement planning, even though retirement sounds like a finance topic. Time is the structure that holds the plan.

- Timers turn effort into a session you can finish today.

- Alarms protect routines when motivation is low.

- Stopwatch sessions make workouts and practice measurable.

- Countdowns create a sense of progress toward a date.

- Duration math supports planning with dates and deadlines.

- Unix time helps when you work with systems, logs, or global teams.

Time.you offers these tools in one place. That makes it easier to stick with a system instead of bouncing between apps. When your planning and your habits live together, follow through is simpler.

Building habits that last, without turning life into a spreadsheet

Retirement planning fails when it feels like punishment. It works when it feels like care for future you. Habits are where that care shows up. You do not need many habits. You need a few that you can keep during busy seasons.

|

Quote to keep: A plan that you revisit beats a plan that you admire. |

Two habit styles are common. One style is calendar driven. The other is trigger driven. Calendar driven habits use a set schedule, like every Sunday evening. Trigger driven habits attach to something that already happens, like after payday or after you brush your teeth. Choose the style that fits your life, not the style that looks best on paper.

Try a short focus session using timer for 25 minutes of admin or money review. Keep the session short. End on time. A short session you repeat builds more momentum than a long session you avoid.

If focus is hard, it helps to understand why. Attention and time pressure affect each other. timers and stopwatches improve focus explains the psychology in a grounded way. It is not about forcing productivity. It is about making effort feel contained.

Retirement budgeting that respects your real life

Budgeting has a reputation for being strict. A better approach is to separate needs, wants, and future support. Future support includes retirement savings, emergency savings, and insurance. The goal is not to remove joy. The goal is to pay yourself in a way that keeps options open later.

One calm method is to define three numbers:

- Baseline cost for a normal month.

- Protected savings that happens even when life is busy.

- Flexible money that you can spend without guilt.

Then review once per month, not every day. A monthly review prevents overthinking. It also keeps you from reacting emotionally to one expensive week.

How to set milestone targets you can actually track

Milestones should be specific enough to measure, but not so strict that you quit when life gets messy. Each milestone works best when it has three parts: a date, a number, and a behavior.

Here is an example:

- Date: end of the next quarter

- Number: emergency fund equals three months of baseline costs

- Behavior: automatic transfer on payday

Then you choose how to track it. Some people like a notebook. Some use a spreadsheet. Some use a calendar reminder. What matters is that you can see it and update it.

If you like the feeling of a visible clock moving toward your goal, use countdown to mark the next check in date. When the check in arrives, you make one decision, not a whole new plan.

Planning across time zones for family, work, and retirement dreams

Retirement plans often include travel, moving cities, or spending time with people in different places. Even before retirement, global teams and long distance families are common. Time zone confusion creates stress and missed moments. It also makes long range planning feel harder than it needs to be.

Time.you exists to remove that friction. It shows the exact time for major cities, countries, and time zones, with atomic clock synchronized accuracy. That level of accuracy is not only for tech. It is also for reliability. When you schedule a habit, a call, or a deadline, you want it to happen when you think it will happen.

If you work with time standards, it helps to understand the basics. You might see military time in travel and logistics. military time references can reduce confusion when booking or coordinating schedules.

Career milestones that often decide retirement timing

Career is not only income. It is identity, community, and daily structure. That is why retirement timing is rarely only about money. Career milestones can either speed up retirement or pull it later.

Common career milestones that affect the plan:

- First role with benefits and retirement contributions

- Promotion that changes your income baseline

- Switch to a new industry with different stability

- Burnout that forces a break

- Starting a business

- Taking time off for caregiving

Each milestone deserves a small review. That review has one job: update your timeline. Your timeline is not a moral scorecard. It is a map.

Family milestones and how to plan without conflict

Family can be the best reason to plan. It can also be the hardest part to talk about. Money can feel personal, even in loving relationships. A timeline helps because it shifts the conversation away from blame and toward dates and needs.

One helpful structure is to hold a short family planning session once per month. Keep it short, around 30 minutes. Set a start time and end time. Use a shared timer so it does not drag. The point is not to solve everything. The point is to stay aligned.

For families that are busy, an alarm can protect this habit. alarm works well for recurring reminders that do not depend on motivation.

Health milestones that shape what retirement feels like

People often talk about money first and health second. In real life, health can decide the shape of retirement. If your energy is low and your body hurts, even a large savings account cannot buy back daily comfort. The goal is not perfection. The goal is steady care.

Track health in simple ways:

- Sleep consistency

- Movement per week

- Strength and mobility

- Stress recovery time

- Medical check ups you actually attend

Time tools help here too. A stopwatch makes workouts measurable without being intense. It can also turn walking into a game. Try stopwatch for a weekly baseline walk, then track how your time changes across months.

|

Quote to keep: Your body is part of your retirement account. |

How to use birthdays as a planning ritual

Birthdays can feel emotional. That is exactly why they can be powerful for planning. One day per year you naturally reflect. Use that moment to update your timeline without drama.

Here is a birthday ritual that stays light:

- Check your age and confirm your next milestone ages.

- Write one win from the past year.

- Write one lesson from the past year.

- Choose one financial action for the next year.

- Choose one health action for the next year.

- Choose one relationship action for the next year.

If you want a playful push to follow through, a visible countdown can keep the year from slipping away. birthday countdown can turn the next birthday into a gentle reminder that time moves, and plans are allowed to change.

Age milestones that affect legal rights and planning

Legal thresholds vary by country and can affect education, work, and retirement benefits. Even if you are not near a threshold, it helps to know what exists. Planning is calmer when you know which dates are flexible and which dates are set by rules.

Voting is one example of a legal age milestone that often changes how people feel about adulthood and responsibility. If you want to see a clear view of how voting ages can differ by place and context, voting eligibility offers a focused reference.

School start age is another milestone that shapes family timelines, childcare costs, and career decisions for parents. school start can help when you are mapping family logistics and long range costs.

Planning the retirement number without getting lost in formulas

People love a single retirement number. It feels clean. Real life is messy. A better approach is to build a range, then narrow it as you get closer. Start with your baseline monthly cost. Add flexibility for health, travel, and support for others. Then test a few scenarios.

A calm set of scenarios could be:

- Simple living, lower travel, stable housing

- Balanced living, some travel, moderate upgrades

- Active living, frequent travel, higher experiences budget

Once you have scenarios, you can connect them to a retirement date, and to a plan for spending. Your plan can shift across the years. Many people spend more in early retirement and less later. Planning in phases reduces fear.

Pre retirement checkups that reduce surprises

The final stretch before retirement tends to be emotional. You have worked for years and want clarity. A checklist can help, but it should not be overwhelming.

Here are the checkups that matter most:

- Debt check: what is left, what must be paid, what can be refinanced

- Budget check: baseline costs and realistic enjoyment costs

- Health check: expected care needs and lifestyle plans

- Housing check: where you want to live and why

- Support check: who depends on you and what help you want to offer

- Purpose check: what you want to do with your time

If you want a reference focused on retirement age planning and the idea of timing, retirement can complement this section by framing retirement in age based milestones.

Purpose milestones that keep retirement from feeling empty

Money and health are the basics. Purpose is the glue. Many people underestimate how much structure work provides. When that structure ends, the days can feel wide and strange. This is not a failure. It is a normal adjustment.

Purpose planning does not need big goals. It needs a few anchors. Anchors can be people, projects, learning, service, creativity, or movement. A useful approach is to plan for three layers:

- Daily anchors that give your day a gentle shape.

- Weekly anchors that connect you to people or projects.

- Seasonal anchors that give you something to look forward to.

A simple timer based routine can support daily anchors. If you enjoy structured focus, a classroom style view can be motivating. classroom timer can help you run a short learning block for reading, language practice, or a hobby session.

How to review your plan on a schedule that feels human

Reviews are where plans come alive. Without reviews, you are just making promises to yourself. The trick is to review often enough to stay aware, but not so often that you get obsessed.

A common rhythm that works:

- Weekly review of habits. Ten minutes. Check what is working and what is not.

- Monthly review of cash flow and upcoming bills. Twenty minutes.

- Quarterly review of bigger goals and timelines. Forty five minutes.

- Yearly review of life direction. One longer session, with kindness.

Set a dedicated day and keep it consistent. If you miss it, reschedule, do not quit. A simple reminder can prevent drift. You can set a recurring ritual using a countdown timer for the quarterly review. countdown timer can make that session feel like an event, not a chore.

Common mistakes that quietly delay retirement

Small choices add up. The patterns below are not about shame. They are about awareness. If you see yourself in one, you can change one step at a time.

- Waiting for clarity before starting. Clarity often arrives after action.

- Saving only when you feel motivated. Automation beats motivation.

- Ignoring health until it becomes urgent. Small routines beat major overhauls.

- Underestimating fixed costs. Fixed costs decide flexibility.

- Planning alone when support would help. A trusted person can reduce stress.

- Overreacting to short term news. A long timeline needs calm actions.

|

Quote to keep: Avoiding the plan does not stop time, it only reduces options later. |

How time measurement helps you save without feeling deprived

Saving can feel like loss. A useful trick is to connect saving to time, not to deprivation. Instead of thinking, I cannot spend this, think, I am buying future time freedom. That shift makes saving feel meaningful.

Try a time based approach:

- Pick one expense that you can reduce without pain.

- Estimate the yearly amount that change saves.

- Translate that amount into months of baseline costs.

- Write the result next to your retirement timeline.

This turns a small habit into a visible chunk of time freedom. When you see the time result, you are less likely to resent the change.

Planning breakpoints with date and time math

Many milestone plans fail because they ignore breakpoints. A breakpoint is a moment when life changes enough that your plan must change too. Examples include a move, a new job, a new dependent, or a health event. You cannot predict all breakpoints. You can plan how you will respond.

A simple response plan:

- Pause and name the change.

- List the next three decisions you must make.

- Set dates for those decisions.

- Remove one non essential task for two weeks.

- Return to your plan with updated numbers.

For the date math side, you can use the same time calculator you used for retirement mapping. It helps you plan decision dates without mental strain, especially when you are stressed.

Tracking milestones in seconds, days, and years

Most of us live in days and months. Tech systems often live in seconds. Both views can be useful. Viewing age in seconds can be surprisingly motivating because it shows how large life really is, and how fast a year can pass when you are busy.

If you want to see that perspective, age in seconds gives a clear number you can reflect on. This is not meant to pressure you. It is meant to remind you that each day is a real unit you can use well.

For practical tracking, the simplest system is still the best. Keep a list of your next five milestones, each with a date, a number target, and a habit. Review monthly. Adjust as needed. Repeat.

Digital time skills that support retirement planning at work

If you work with data, logs, apps, or international teams, time formatting matters. Mistakes in time calculations can cause missed deadlines or billing errors, which can ripple into stress. Learning the basics of how systems track time can protect you.

Unix time is one common standard, especially in computing. If you ever need to convert timestamps or understand logs, unix tools can help. Even if you are not a developer, basic familiarity can reduce confusion in many workplaces.

Milestones for pet owners planning long term routines

Pets are family for many people. Planning for them is part of life planning. They also influence daily routines, travel freedom, and budget needs. If you care for a pet, building predictable routines can reduce stress now and later.

Some people enjoy tracking pet age milestones for health checkups and lifestyle changes. If that fits your life, dog cat age provides a friendly reference for understanding pet age comparisons. It is a small detail, but small details often make routines easier to keep.

Milestone planning for students and young workers

If you are early in life, retirement can feel far away. That does not mean you should ignore it. It means you should keep it simple. Your best milestone is not a huge retirement number. Your best milestone is building habits that create options.

Start with these milestones:

- Know your exact age and a few future checkpoint ages.

- Build an emergency buffer, even if small.

- Learn one skill that increases income potential.

- Practice one health routine that you can keep.

- Review quarterly and adjust your next step.

These milestones are light enough to carry. They still compound over time.

Milestone planning for mid career adults with many responsibilities

This season can be intense. You may be building a career while raising children, supporting parents, or managing debt. Perfection is not realistic. Your plan should protect basics and reduce future stress, not add to your workload.

Focus on three goals:

- Cash flow stability through reduced expensive debt and predictable bills.

- Protected savings that happens automatically, even if it is modest.

- Health stability through consistent movement and sleep.

Use time tools to reduce thinking. A short timer session once per week can handle admin tasks. If you need a specific study style focus session for exam prep or professional training, exam timer can keep sessions structured and finite.

Milestone planning for people approaching retirement age

This season brings clarity and pressure at the same time. Choices now can have larger impact. The most helpful move is to reduce unknowns. Unknowns create fear. Reducing unknowns creates calm.

Questions to answer in this season:

- What is my baseline monthly cost today, and what might change later?

- Which fixed costs can I reduce, and which do I accept?

- What health costs should I plan for?

- What work options do I have if I want to ease into retirement?

- What brings meaning to my week?

Then put dates on decisions. A decision without a date becomes a worry. A decision with a date becomes a task.

How to keep a retirement plan flexible when life changes

Flexibility is not a lack of commitment. It is respect for reality. Your plan should allow for surprise. It should also allow for joy. That means building buffers, not only money buffers but time buffers and energy buffers.

Practical flexibility tips:

- Keep an emergency fund that matches your life risk level.

- Limit fixed costs when you can.

- Maintain skills that allow income in different ways.

- Protect health routines, even small ones.

- Review milestones quarterly and revise without guilt.

Flexibility is easier when you have a simple system you trust. Time tools can serve as that system because they reduce the mental load of planning. You do not have to hold every date in your head.

A listicle of practical milestone ideas you can start this week

Here are small, concrete milestone ideas that create momentum. Pick two, then keep them for a month before adding more.

- Set one weekly 25 minute session to check money basics.

- Create one savings transfer that happens automatically.

- Choose one health habit that takes under ten minutes.

- Write your next five milestones on paper and post them where you will see them.

- Plan one learning block per week for a skill that helps your future income.

- Set one family planning check in with a clear start and end time.

- Pick one future date, then count back the steps to reach it.

- Schedule one rest block each week to protect energy.

- Track one routine with a simple timer or alarm instead of willpower.

- Review your timeline on your birthday and adjust kindly.

Milestone table you can copy into your own plan

This table is designed to be readable and practical. It pairs common milestones with a time tool that makes the milestone easier to act on. Use it as a menu, not as a checklist you must finish.

| Milestone | What to decide | Time tool support | Tiny action |

|---|---|---|---|

| Next paycheck | How much to save first | Use an alarm for the review day | Set an automatic transfer |

| Next quarterly review | Which goal matters most now | Use a countdown timer to mark the session | Write one decision you will make |

| Next birthday | Which milestone age is approaching | Use a birthday countdown to track time | Update your top five milestones |

| Training season | Which skill raises options | Use an exam style timer for study blocks | Do one focused session per week |

| Health baseline month | What you can keep steady | Use a stopwatch to track a walk time | Repeat the same route weekly |

| Retirement target date | What must be true by then | Use a time calculator for date math | List the next three steps |

Planning your week number, calendar rhythm, and review days

People often set goals but forget to set a rhythm. Rhythm is the invisible support. It is how you keep going when life gets busy. If you want your plan to last, tie it to a calendar rhythm that you can repeat.

Some people prefer weekly planning. Others prefer a monthly reset. If you like weeks as your unit, the week number can be a clean way to keep track of progress across the year without needing to remember exact dates. week number can help you label your plan in a way that feels orderly.

If you prefer a calendar view for your review rituals, calendar tools can support your scheduling and help you keep your plan visible without constant effort.

Putting it all into a single page plan

A pillar plan should fit on one page. If it grows beyond that, it becomes something you avoid. You can keep a detailed version elsewhere, but your main plan should be readable in one sitting.

Here is a one page structure you can copy:

- My retirement target range: write a start and end month and year.

- My next five milestones: each with date, number, habit.

- My protected savings habit: what happens automatically.

- My health anchor habit: what I can keep in busy seasons.

- My review rhythm: weekly, monthly, quarterly, yearly dates.

- My support list: people, resources, professional help if needed.

Then keep it visible. A plan you see becomes a plan you use.

A closing thought for the road ahead

Your milestones do not exist to pressure you. They exist to support you. Retirement becomes less scary when you treat it as a series of small, human steps. Choose dates you can revisit, habits you can keep, and tools that reduce mental load. Time.you can help you measure and manage the parts of the journey that are easiest to ignore: the minutes, the days, and the patterns that quietly build a future you will be glad to meet.